"In my view, this is what GIS (geographic information system software) is for. I pray that this analysis is used for some form of social justice."

New Racial Meanings of Housing in America

Selected

References

Manuel B. Aalbers, ed. (2012). Subprime Cities: The Political Economy of Mortgage Markets. Hoboken, NJ: Wiley.

David Harvey (1974). "Class-monopoly rent, finance capital and the urban revolution." Regional Studies 8(3-4), 239-255.

David Harvey (2011). The Enigma of Capital and the Crises of Capitalism. New York: Oxford University Press.

Michael Omi and Howard Winant (1994). Racial Formation in the United States: From the 1960s to the 1990s. New York: Routledge.

Anita F. Hill (2011). Reimagining Equality: Stories of Gender, Race, and Finding Home. Boston, MA: Beacon Press.

Phil Ashton (2009). "An Appetite for yield: The anatomy of the subprime mortgage crisis." Environment and Planning A 41(6), 1420-1441.

Gary A. Dymski (2009). "Racial Exclusion and the Political Economy of the Subprime Crisis." Historical Materialism 17(2), 149-179.

Kathleen C. Engel and Patricia A. McCoy (2011). The Subprime Virus: Reckless Credit, Regulatory Failure, and Next Steps. New York: Oxford University Press.

Susan Saegert, Desiree Fields, and Kimberly Libman (2011). "Mortgage Foreclosures and Health Disparities: Serial Displacement as Asset Extraction in African American Populations." Journal of Urban Health 88(3), 390-402.

Dan Immergluck (2009). Foreclosed: High-Risk Lending, Deregulation, and the Undermining of America's Mortgage Market. Ithaca: Cornell University Press.

Jeff Crump, Kathe Newman, Eric S. Belsky, Phil Ashton, David H. Kaplan, Daniel J. Hammel, and Elvin Wyly (2009). "Cities Destroyed (Again) for Cash: Forum on the U.S. Foreclosure Crisis." Urban Geography 29(8), 745-784.

Elvin Wyly and C.S. Ponder (2011). "Gender, Age, and Race in Subprime America." Housing Policy Debate 21(4), 529-564.

Excerpt presented at "Context and Consequences: The Hill-Thomas Hearings Twenty Years Later." Washington, DC: Georgetown University School of Law, October 6. The text is here, and the images are here, and the webcast of the entire event is here. Professor Emma Coleman Jordan introduces our panel in Part I around the 1:54 mark.

Elvin Wyly (2010). "Good Data, Good Deeds." Testimony presented at the Federal Reserve Bank of San Francisco, Community Advisory Board hearing, August 5. Audio here or here, full transcript of the entire hearing here.

Financial Crisis Inquiry Commission (2011). Final Report of the National Commission on the Causes of the Financial and Economic Crisis in the United States. Washington, DC: U.S. Government Printing Office.

Emily Rosenman and Sam Walker (2012). A Root Canal of Community Development: A Preliminary Analysis of the Post-2008 Geography of Foreclosure Demolitions in Cleveland, Ohio. Vancouver, BC: Department of Geography, University of British Columbia.

Ruthless

"Mapping foreclosures in an American Metropolis"

This map shows pre-foreclosure lis pendens notices in Essex County, New Jersey, between 2004 and 2008. Color codes refer to local indicators of spatial association: shades of red and blue indicate statistically significant spatial clusters of the length of "survival" of a loan -- the time from origination to slipping into default.

See also Ken Zimmerman, Elvin Wyly, and Hilary Botein (2002). Predatory Lending in New Jersey: The Rising Threat to Low-Income Homeowners. Newark, NJ: New Jersey Institute for Social Justice and Kathe Newman and Elvin Wyly (2004). "Geographies of Mortgage Market Segmentation: The Case of Essex County, New Jersey." Housing Studies 19(1), 53-83.

The Racialized Urban System of American Subprime Capital

Special issue of Housing Policy Debate, based on evidence from the National Mortgage Data Repository

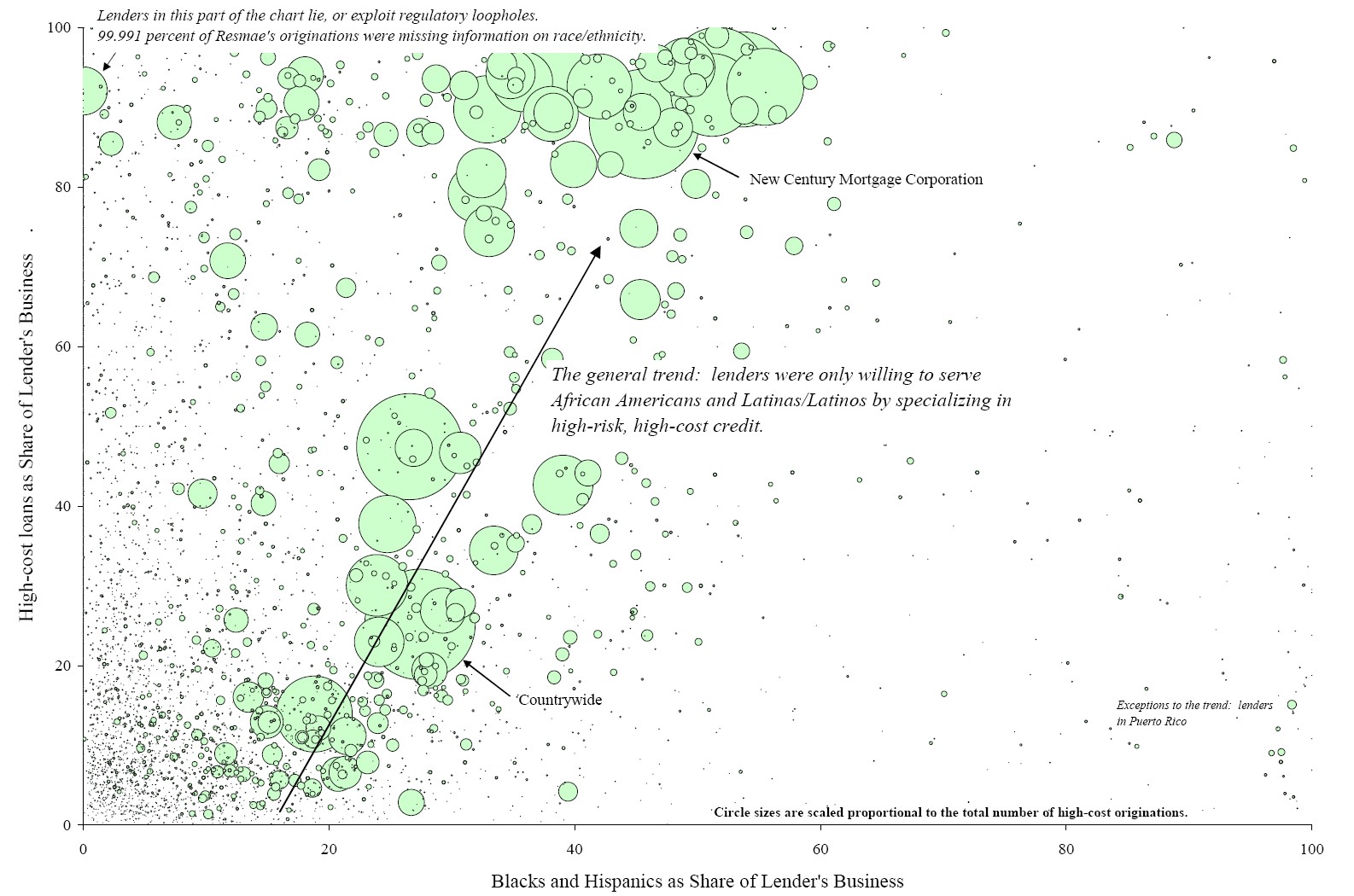

At the same time, the structures of American federalism and banking law allowed capital to evade limits on abusive behavior. Some of those limits -- from the populist backlash against farm foreclosures in the nineteenth century to the Depression bank reforms and the Civil Rights fair housing struggles -- were explicitly dismantled through deregulation in the 1980s and 1990s. But lenders also began to exploit loopholes between state and federal rules, and they organized their operations in ways that achieved a stealth repeal of fair lending legislation. Regulations requiring equal treatment of all borrowers, for example, are easy to skirt if marketing practices and broker referral networks ensure that different groups of consumers wind up at different kinds of specialized subsidiaries. Everyone who goes to the easy-credit storefront predator gets a bad deal; but the entire business is designed so that African Americans and Latinas/os are pushed to these kinds of subprime operations, while competitive, prime credit retains its longstanding white privilege.

Here's one view of the racialized landscape of lender subsidiaries, at the peak of the boom in 2006. For the full worksheet of all 8,657 lenders and subsidiaries reporting data under the Home Mortgage Disclosure Act, see this.

Supplementary images, references, and data.

Elvin Wyly, C.S. Ponder, Pierson Nettling, Bosco Ho, Sophie Ellen Fung, Zachary Liebowitz, and Dan Hammel

Odds ratios from logistic regressions, compared to Non-Hispanic Whites, after controlling for income, loan type and purpose, loan to income ratio, and all other publicly available independent variables.

|

|||||||

African American

|

Hispanic

|

||||||

Segmentation

|

Denial

|

Segmentation

|

Denial

|

||||

2004

|

2.93

|

1.80

|

1.76

|

1.22

|

|||

2005

|

3.16

|

1.73

|

2.34

|

1.25

|

|||

2006

|

3.08

|

1.86

|

2.41

|

1.43

|

|||

2007

|

2.51

|

2.12

|

1.85

|

1.72

|

|||

2008

|

1.94

|

2.47

|

1.51

|

1.94

|

|||

2009

|

1.65

|

2.52

|

1.35

|

1.95

|

|||

2010

|

1.45

|

2.40

|

1.44

|

1.77

|

|||

Data Source: Calculated from loan-level records from FFIEC (2005-2011).

|

|||||||

...yet while African American and Latina/o people and places faced disproportionate exploitation, there were simply not enough black and brown people to satisfy the "appetite for yield" of Wall Street's securitization machine (Ashton, 2009). In the housing boom, the "innovations" of predatory practices perfected during years of extraction from minority urban neighborhoods were deployed across a broader, multiracial array of sunbelt suburban growth frontiers. The evolving yet enduring whiteness of American housing finance conditioned the way Wall Street pursued economies of exploitative scale.

Predatory mortgage capital created new racialized inequalities between "good" and "bad" credit, but never entirely erased the old disparities of racial exclusion. At the peak in 2006, African American borrowers were three times more likely than otherwise identical non-Hispanic Whites to receive high-cost mortgages; for Latinos, the disparity was 2.41.

*Note that since tract conditions reported in HMDA are based on 2000 Census data, it is possible that some of the high-cost loans going into tracts that appear to be middle- or high-income white neighborhoods are targeted to African American or Latino/a borrowers in expanding peripheral suburban neighborhoods. See, for example, Alex Schafran and Jake Wegman, "Restructuring, Race, and Real Estate: Changing Home Values and the New California Metropolis, 1989-2010." Urban Geography, forthcoming, October 2012.

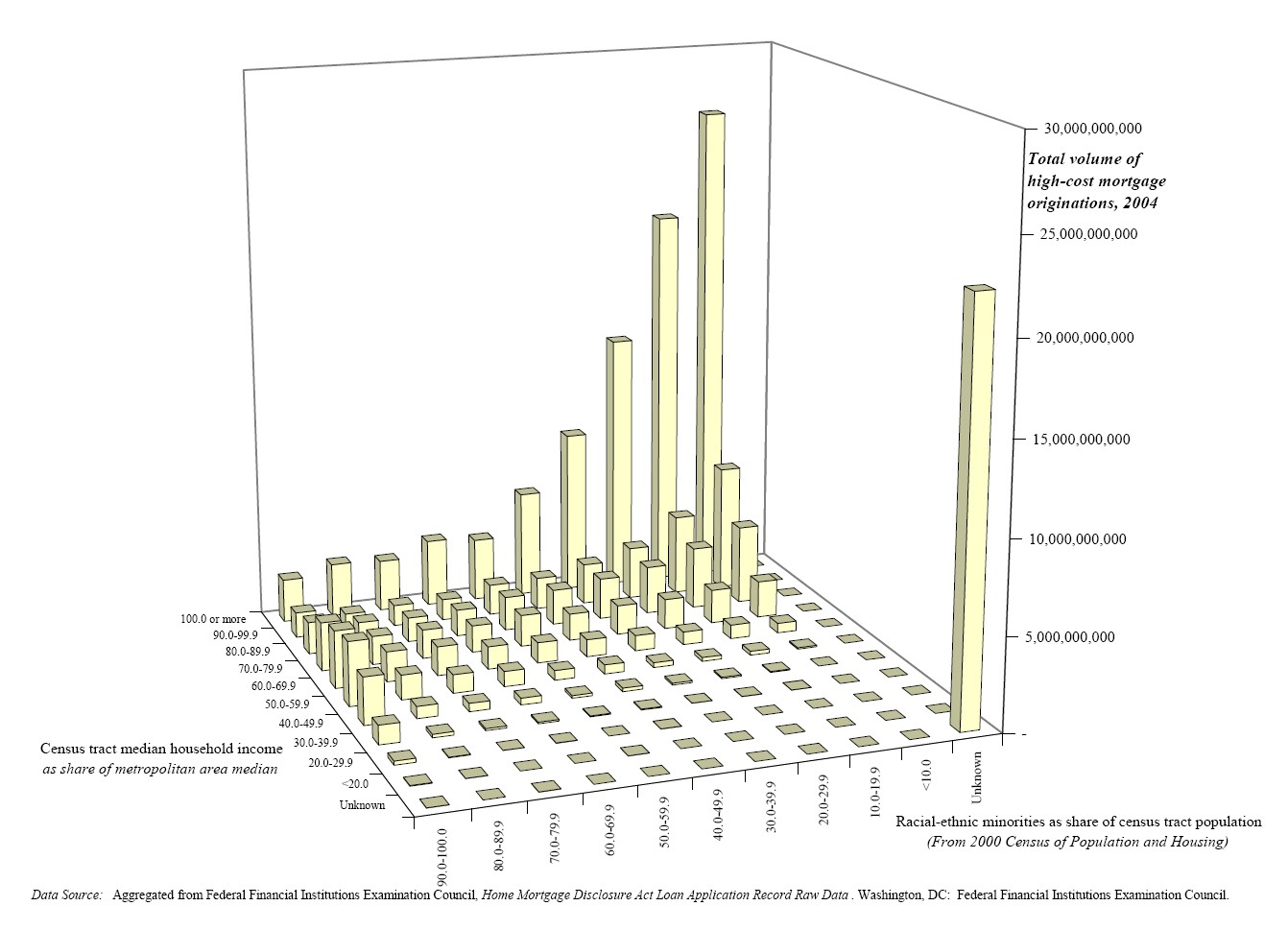

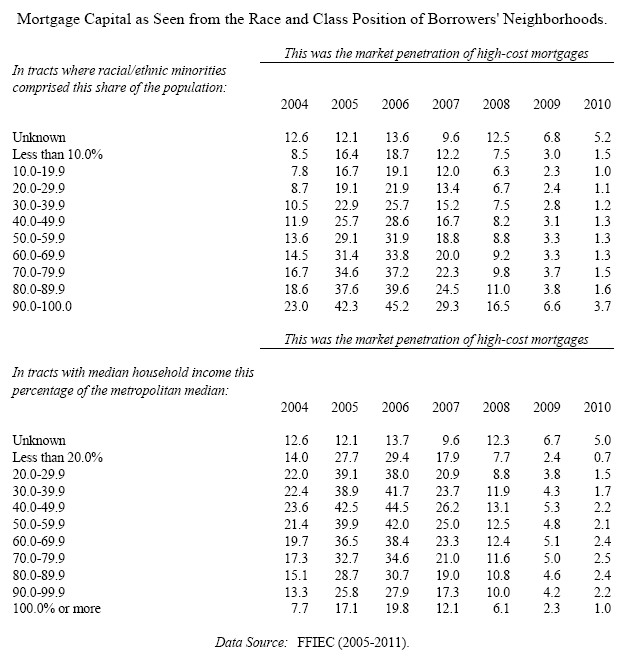

Racial disparities are also inequalities of place: at the peak, the market penetration of risky subprime lending in "all minority" neighborhoods (45.2 percent) was 2.44 times the rate (18.7 percent) in all-white neighborhoods.

Racial disparities are intensified with social constructions of gender, household relations, and age. Compared with Non-Hispanic White traditional couples, single-applicant African American women are 4.84 times more likely to wind up with high-cost mortgages; compared with borrowers under age 30, borrowers 65 years and older are 15 times more likely to be African American women, after accounting for differences in income, net worth, and loan purpose.

See Elvin Wyly and C.S. Ponder (2011). "Gender, Age, and Race in Subprime America." Housing Policy Debate 21(4), 529-564.

"...debt robs... debt also disciplines."

All of these factors reflect and reinforce a complex, racialized urban system. Distinctive urban and regional histories of growth and suburbanization, racial and ethnic change, and immigration interact with state laws and lending industry strategies of competitive position and local market segmentation.

...and thus we now have an evolving urban system of foreclosures, dispossessions, evictions, and demolitions on a scale not seen since the 1930s. The violence in the housing market, Eric Belsky predicted in a panel discussion in early 2008, would be like something out of a Sam Peckinpah movie.

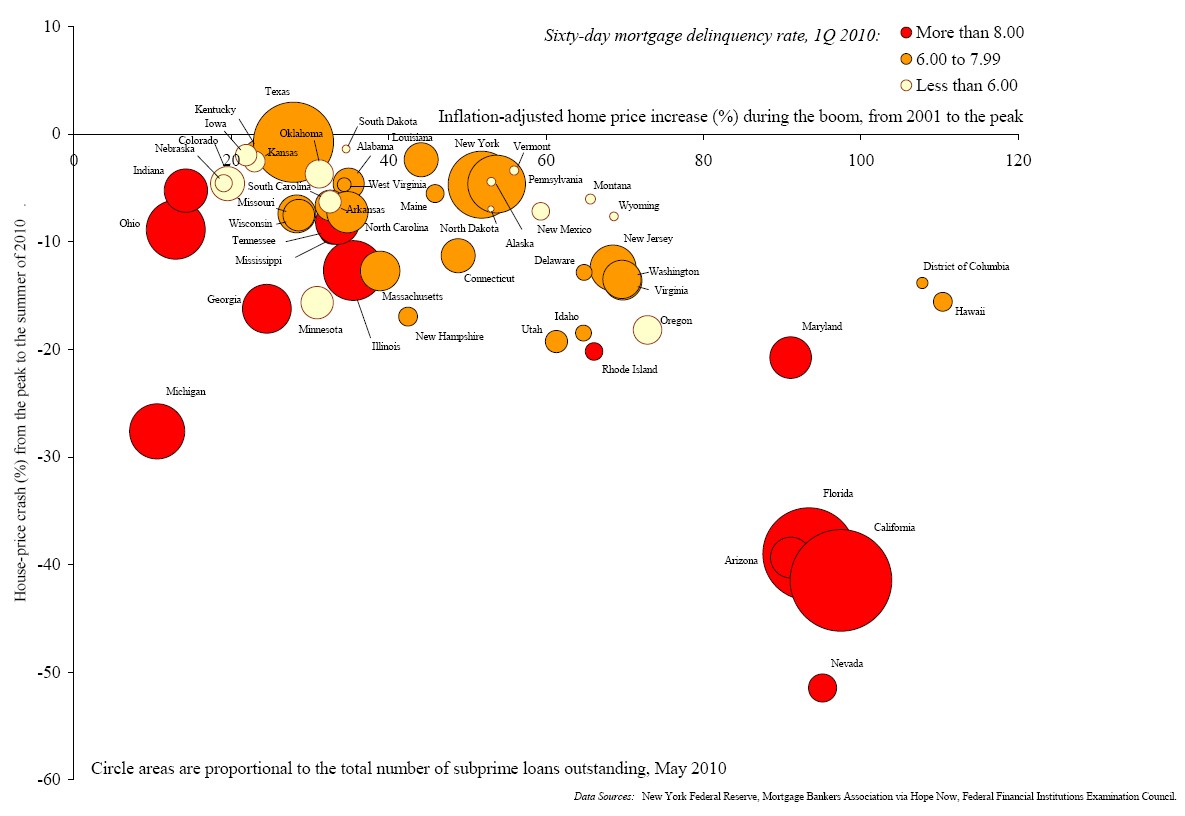

Disastrous State of the States